Revolving debt is a flexible financing option that allows companies to borrow and repay funds within a predefined credit limit. Let's explore the types of revolving credit, their costs, purposes, and how to calculate the need for and utilization of revolving credit to manage cash flow effectively.

Types of Revolving Credit:

1. Revolving Line of Credit: A pre-approved credit line that allows borrowers to draw funds as needed and repay them, with interest, over time. It provides flexibility for short-term financing needs and is often used for working capital management.

2. Credit Cards: Revolving credit cards allow users to make purchases up to a certain credit limit and repay the balance in full or over time, with interest. They are widely used for both personal and business expenses and offer convenience and flexibility in spending.

Cost of Revolving Credit: The cost of revolving credit typically includes:

· Interest: Charged on the outstanding balance at the prevailing interest rate.

· Fees: Such as annual fees, transaction fees, and late payment fees.

Purposes of Revolving Credit:

1. Working Capital Management: Revolving credit helps companies manage cash flow fluctuations by providing access to funds for day-to-day operations, such as inventory purchases, payroll, and operating expenses.

2. Emergency Funding: It serves as a safety net for unexpected expenses or revenue shortfalls, ensuring that companies can meet their financial obligations even during challenging times.

Calculating the Need for Revolving Credit:

To determine the need for revolving credit and its utilization, companies can use a cash flow forecasting model. Here's how it works:

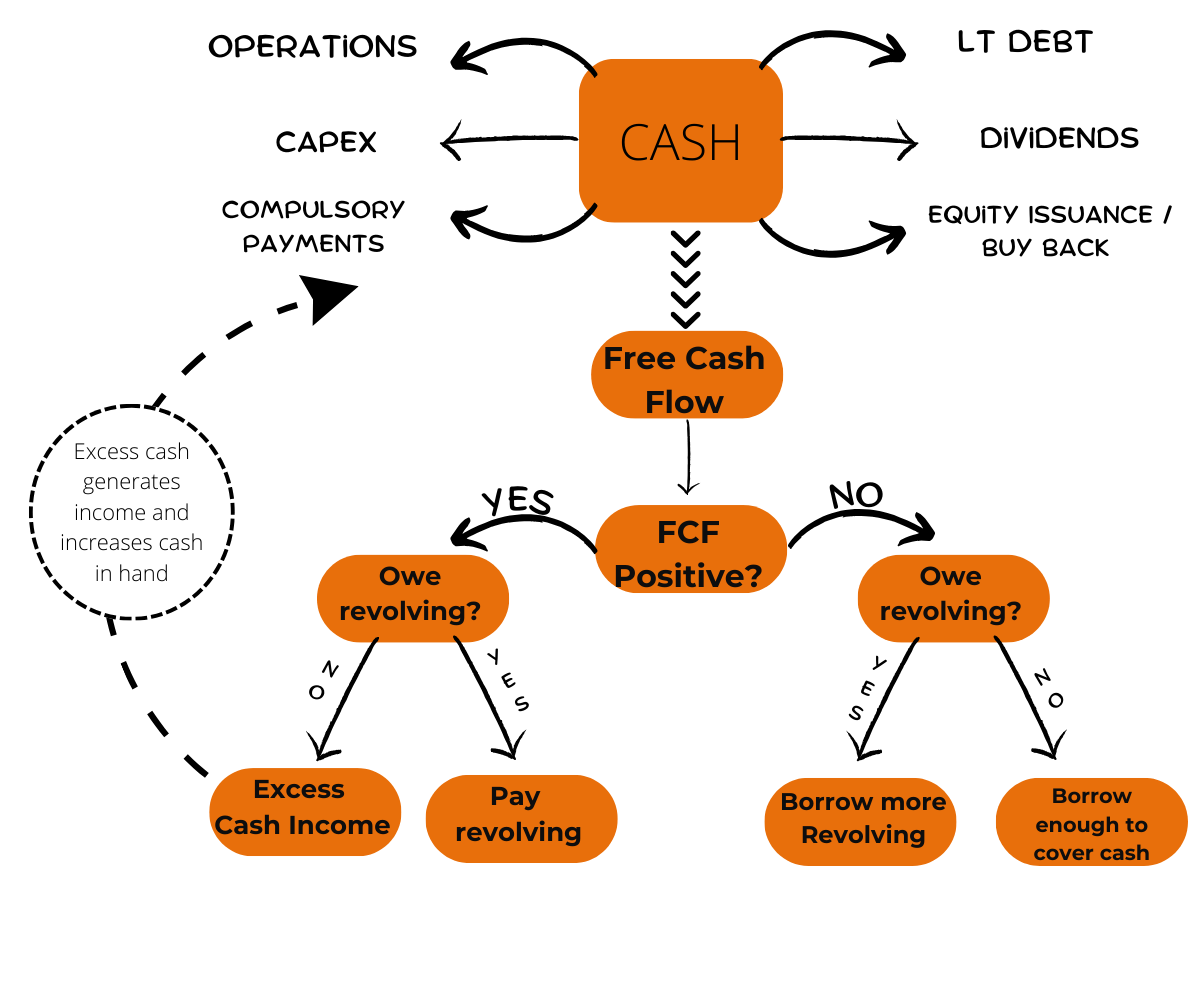

1. Create a Free Cash Flow Forecast: Forecast the cash inflows and outflows for a specific period, considering factors such as sales revenue, operating expenses, capital expenditures, and debt repayments.

2. Assess Cash Requirements: Analyze the projected cash flow to identify periods of cash shortfall or surplus. Determine the amount of revolving credit needed to cover shortfalls and maintain adequate liquidity.

3. Automatic Issuance and Repayment: Establish automated processes to draw funds from the revolving credit line when needed, based on predetermined triggers or thresholds. Similarly, set up automatic repayments when excess cash is available to minimize interest costs.

By effectively utilizing revolving credit, companies can maintain financial flexibility, manage cash flow fluctuations, and ensure continuity in their operations, even in challenging economic conditions.

Enhancing Financial Models with an Automatic Debt Revolver/Cash Sweep

Step 1: Define Key Parameters

Start by setting up the necessary inputs in your model:

- Maximum Revolver Limit: The maximum amount that can be borrowed at any given time.

- Interest Rate: The rate at which borrowed funds will accrue interest.

- Initial Cash Balance: Starting cash before any transactions.

Step 2: Model the Cash Flows

Project your operating cash flows, including all expected inflows and outflows. This should reflect realistic scenarios over the forecast period.

Step 3: Implement the Revolver Mechanism

In your cash flow model, use the following formulas to calculate the revolver borrowing and repayments:

- Net Cash Flow (monthly): =Inflows - Outflows

- Cumulative Net Cash (end of month): =Previous Cumulative Net Cash + Net Cash Flow

Step 4: Calculate Revolver Draws and Repayments

Use Excel’s MIN and MAX functions to determine monthly revolver activity:

- Revolver Draw: =MAX(0, -Cumulative Net Cash) This formula ensures additional funds are drawn only when there is a deficit.

- Revolver Repayment: =MIN(Cumulative Net Cash, Previous Revolver Balance) This ensures that any surplus cash is used to repay the revolver up to the existing balance.

Step 5: Update the Closing Cash Balance

Finally, calculate the closing cash balance considering the revolver activity:

- Ending Cash Balance: =MAX(0, Cumulative Net Cash + Revolver Draw - Revolver Repayment)

Advantages of an Automatic Revolver in Your Model

Integrating an automatic debt revolver/cash sweep in your financial models offers several strategic advantages:

- Liquidity Management: Automatically adjusts your cash position to avoid deficits, ensuring liquidity without manual adjustments.

- Interest Optimization: Minimizes interest expenses by using surplus cash to pay down the revolver promptly when excess funds are available.

- Scenario Analysis: Enhances the realism of financial forecasts and stress tests by dynamically adjusting to various cash flow scenarios without showing unrealistic negative cash balances.

By incorporating an automatic debt revolver/cash sweep into your financial models, you equip your analysis with a robust tool for managing liquidity efficiently. This setup not only prevents the pitfalls of negative cash balances but also optimizes interest costs, contributing to a more accurate and realistic financial planning process. As you refine your model with these advanced functionalities, your financial forecasts become a more reliable compass guiding your business decisions.