Forecasting fixed assets and depreciation is a critical aspect of financial planning and analysis (FP&A) within any organization. Whether you're a finance professional, a business owner, or an investor, understanding how to accurately predict the future value of fixed assets and their corresponding depreciation is essential for making informed decisions. In this article, we'll delve into the intricacies of forecasting fixed assets and depreciation within the framework of a three-statement financial model, including intangible assets such as software and the calculation of amortization.

Understanding Fixed Assets and Depreciation: Fixed assets, also known as property, plant, and equipment (PP&E), are long-term tangible assets used in the operations of a business to generate revenue. Examples include buildings, machinery, vehicles, and equipment. These assets are expected to provide economic benefits over multiple accounting periods.

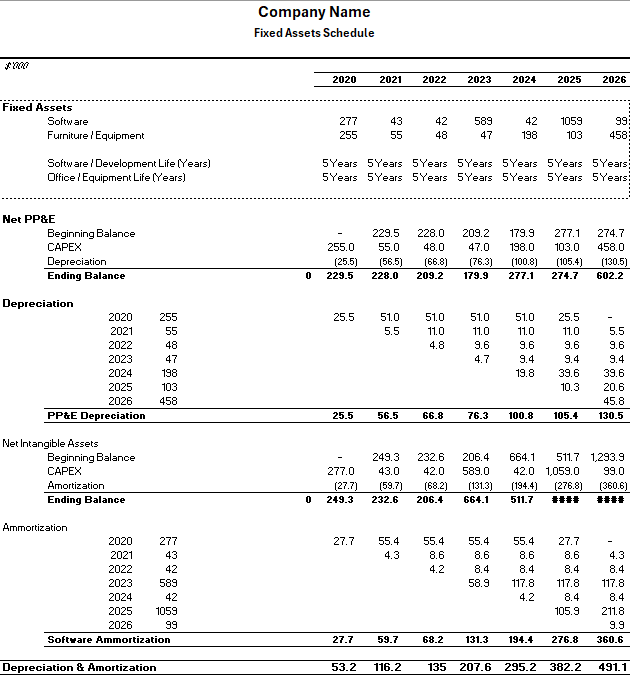

Depreciation, on the other hand, represents the systematic allocation of the cost of a fixed asset over its useful life. It reflects the gradual wear and tear, obsolescence, or expiration of the asset's value over time. Depreciation expense reduces the book value of fixed assets on the balance sheet and impacts the income statement by reducing net income.

Forecasting Fixed Assets: Forecasting fixed assets involves estimating the future additions, disposals, and changes in existing assets based on strategic plans, capital expenditure projects, and operational needs. Here's how to approach it:

- Review Historical Data: Start by analyzing historical trends in fixed asset additions and disposals. Look at past capital expenditure budgets, investment decisions, and industry benchmarks to identify patterns and drivers.

- Consider Business Plans: Understand the company's strategic objectives and growth initiatives. Evaluate upcoming projects, expansions, and investments that may require additional fixed assets.

- Utilize Operating Metrics: Use operational metrics such as sales growth, production capacity, or asset turnover ratios to forecast the demand for new fixed assets. For example, a company experiencing rapid sales growth may need to invest in additional manufacturing equipment.

- Factor in Economic Conditions: Consider macroeconomic factors such as interest rates, inflation, and industry trends that could impact the demand for fixed assets. Economic downturns may lead to reduced capital spending, while favorable conditions may stimulate investment.

- Model Different Scenarios: Develop scenarios to account for varying levels of capital expenditure and investment priorities. Sensitivity analysis can help assess the impact of different assumptions on fixed asset forecasts.

Forecasting Depreciation: Once fixed assets are forecasted, the next step is to estimate depreciation expense. Depreciation methods such as straight-line, declining balance, or units of production can be used based on the nature of the asset and accounting standards. Here's how to forecast depreciation:

- Select Depreciation Method: Choose an appropriate depreciation method based on industry practices, tax regulations, and management preferences. Consider the asset's expected pattern of use and technological advancements.

- Determine Useful Life: Estimate the useful life of each fixed asset, considering factors such as wear and tear, technological obsolescence, and legal or contractual limitations. This will vary for different types of assets.

- Calculate Depreciation Expense: Apply the chosen depreciation method to each fixed asset to calculate annual depreciation expense. Ensure consistency with accounting policies and standards.

- Account for Residual Value: Consider the residual or salvage value of the asset at the end of its useful life. This represents the estimated value that the asset can be sold for after depreciation. Adjust depreciation calculations accordingly.

- Consider Intangible Assets: In addition to tangible fixed assets, consider intangible assets such as software licenses, patents, and copyrights. Amortization is used to allocate the cost of these assets over their useful lives, similar to depreciation for tangible assets.

Forecasting fixed assets and depreciation is a crucial component of financial modeling and FP&A processes. By understanding the drivers of fixed asset investment, analyzing historical data, and applying appropriate depreciation methods, finance professionals can develop accurate forecasts that support strategic decision-making and financial planning. A robust three-statement financial model that incorporates forecasted fixed assets and depreciation enables stakeholders to evaluate the long-term financial health and sustainability of the business, including both tangible and intangible assets.

Download the Excel File here: